The ad industry is facing the dawn of a new era. Online ad channels and proliferate attract more of the advertising budget. Data has evolved into new advertising, the game changer for targeting and processing alongside advertising tech.

New advertising heavyweights have started. The structural transition is set to continue as the ad industry changes dramatically. Explore this article to learn more about a market tracker and how the ad industry is changing right away in this article.

Ad Market Tracker: Ad Spending Measurement of All Media

The U.S. advertising marketplace contracted by almost 12% a year ago, marking its decline by a double-digit rate since 2020, according to MediaPost analysis of information from Standard Media Index’s U.S. Ad Market Tracker.”

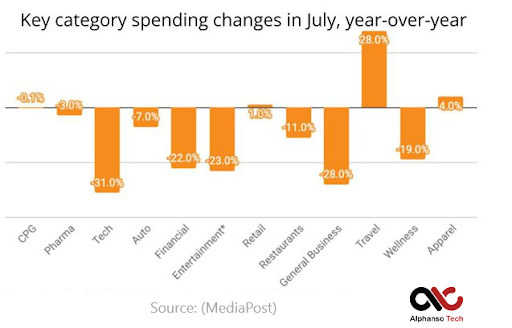

Compared to 2020 data which was the tail-end of the pandemic ad recession, the United States ad market was up 29%. Tiny ad categories continued to sustain ad spending better than the largest ones. The top 10 ad categories declined 14% year-on-year ad spending, and all categories contracted by around 11%.

SMI’s analysis of the specific categories, core data, and more showed mixed results, however overwhelmingly contracting ones. Over than apparel 4%, retail +1%, and travel +28%, the other categories declined, although customers’ packaged goods slid only .1%. As the recent earnings of the social media companies have all pointed to, we’re in an impression recession.

The combo of an enormous glut, ad inventory inflation, and changing consumer behavior has assembled a rising misery index in the ad sales biz. An upfront for O.G. media companies such as NBCU and Disney artificially masked an apparent trend toward reduction in the ad purchasing community.

The tremendous ad commitments in the ultimate irony in the Upfront are solid indications of a more considerable ad downturn than what we see in 2023; these chips on premium impressions are akin to saving accounts against future risk when you dig into the quality of those who aren’t ad dollars.

Travel is a category that shows growth as it shows new-fangled, “going out of the house” things. However, the Media & Entertainment dropped by almost 23%, representing the industry sales ads feeling bearish, and drops in Tech and Financial indicate what can be termed as “bad shit ahead” in tech terms.

What Has Affected the Ad Industry?

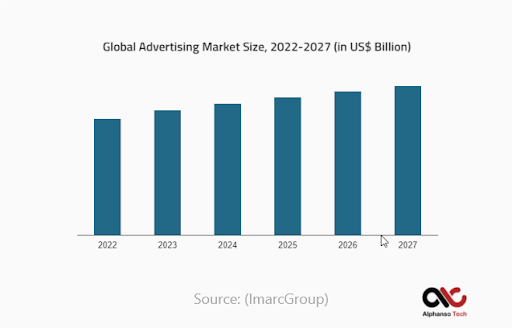

The advertising market globally reached around US$ 590.3 Billion in 2021. The IMARC Group report shows that the market is expected to reach around $ 792.7 Billion by 2027, growing at a 5% CAGR between 2022 and 2027. T.V. ads dominate the market, holding the majority of the market share. This can be attributed to T.V. prevalence, which made them one preferred advertising mode.

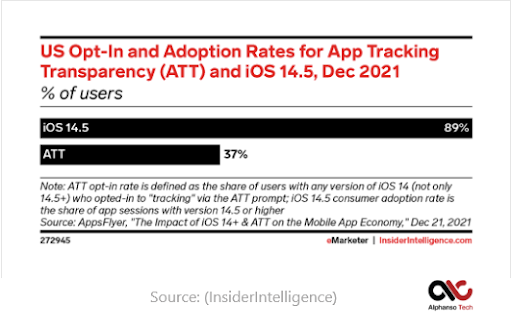

The impression recession hit social and mobile hardest; those who advertised through video are moving off phones and CTVs, whereas social media is a bottomless hellhole for advertisers. When Apple’s AppTrackingTransparency (ATT) update changed mobile advertising dramatically, the industry began to stabilize, whereas mobile ad spending was rising.

Just a month after ATT was launched, users can opt in or out of having their info tracked. The opt-in rate was lower than 23%; however, most apps show the tracing pop-up, and under 50% of users have opted in.

Opt-in rates are higher than the explosive predicted earlier; more users are open to the tracking idea if an app presents them with the option as early as possible. The competition for CPMs and eyeballs is more fierce in 4Q and 2023 compared to the media history.

Come 4Q, when both Netflix and Disney flood the zone with billions of premium impressions on CTV. The extensive media ecosystem officially has a glut of inventory it couldn’t fill at the prices they expect; all ad platforms will be competing with those mega-platforms, including Amazon, Apple, Netflix, Microsoft, Google, and Meta.

More than having a programmatic reach is needed to compare the price or share with platforms that control the mind-shares of customers. However, to compete for the budgets in the Impression Recession, all the players must provide excellent data, proof of efficacy, nimble models, and premium environments.

Ending Note

Continuous increase in media and entertainment expenditure is experienced globally. This indicates rising consumer expenditure capacity for subscribing to magazines and newspapers, acquiring internet access, T.V. and radio, and video gaming. Advertising brands opt for new and effective ways to attack customers’ attention.

Many are choosing to advertise on a video streaming platform like Netflix. They are choosing to advertise in the middle, before, or after the video streaming content; you can also prefer to do the same.